It’s a general problem in real estate now; commercial and residential.

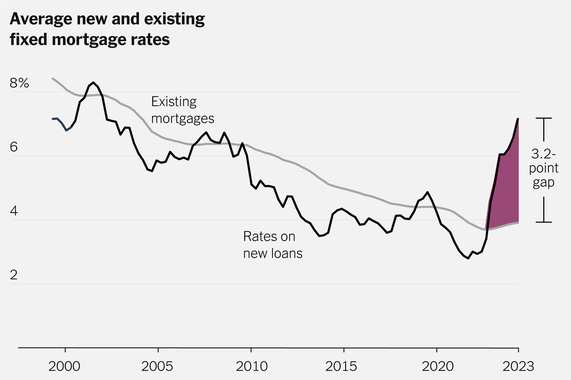

Everyone who was able to refinance to low mortgage rates locked them in. That means that just about anyone who wants to roll over a real estate investment has to take a huge hit in the process. Those rollovers are normally a big part of liquidity and they’ve all dried up.

Its less of a problem of lock in here in Australia. Our rates tend to only be fixed for the first few years. Then you go to the variable rate. We have an opposite problem, where we have what’s known as a mortgage cliff. People who signed up at affordable repayment amounts end that lock in period and have payments jump significantly. Some are forced to sell.

Being locked in seems better than being forced to sell.

Yes, just America was affectednbynthe global financial crisis. Unless you mean the sub prime rates, which ISNA different thing than fixed rates. Usually those on a sub prime rate are on a higher rate not lower.

Here in Germany you can decide how long you want your rates to be fixed, with the tradeoff being that longer times of fixed rates usually have slightly higher rates (in German its Zinsbindung).

I am lucky and happy that I chose to do 30 years fixed rates, after those 30 years I only have like 2k€ left anyway, so it doesnt matter what rates I get then really.

People forget … If you refinance you are essentially selling the house to yourself with the lower rate, but Mr. Taxman will up your taxes to the current market value of your home, which is ridiculously high right now. Any savings in interest goes back into higher taxes. And now you will need more expensive insurance to cover the increase in home value.

This is not how things work in the US. At least not in the states that I’ve lived in: TX, CA, IL.

My current state, TX, regularly updates the property value assessment, so even if I don’t refinance, my property taxes goes up. With homestead exemption, the rise is capped at 10%, but over 2-3 years, it easily catches up to the market value.

But if you’re in CA or NV, that value assessment increase is capped at something like 2% or 1% annually, respectively. (Proposition 13) Creating situations where homes purchased 20 years ago are still paying really low property taxes compared to today’s buyers.

Isn’t that the way it should be? In Florida it’s capped low per year also…you bet the county raises it the max each year. My 95 year old neighbor has a yearly tax bill of 590, mine was 6k. If I stay in my house 50 years, my tax bill will be 1 tenth that of the new owners too.

Its good and bad. I’m conflicted about it, because I think everyone should pay a fair share of the property tax. The person that moved in 20 years ago and the person that moved in yesterday should shoulder the same amount of burden if their properties are equivalent.

But I also think its stupid that my property tax goes up just because some idiot decided to overpay for the house a few houses down the street.

I simply don’t like the idea that the property tax is tied directly to the appraised value of my house. It should really be tied to the size of the land that I am occupying and the total cost of running the city/county that I am in. If I build a fancy shed (insert any structure here) in my backyard, that shouldn’t really cause my taxes to go up even if it increases the value of my property. The only exception is if I change the dwelling type. If it goes from a single family home to a multifamily unit, then definitely the tax rate should be reevaluated, if it is using the infrastructure more.

My wife and I LOVE our house and don’t want to leave, but we definitely thought it was going to be a starter home. We straight up could not afford the mortgage payments anywhere else at today’s rates, even in a much smaller house

I couldn’t afford to buy the house I currently live in, today. The “value” of my house almost doubled in value, and interest rates are close to triple what I have now. There is no way my family is going to move out, it’s pretty stupid that an upgrade of a home, in terms of dollar value, would put me somewhere much smaller.

Are we like not even allowed to talk about renting out our home in order to upgrade or something? That’s the play right now. Net present value of your almostfree money is maximized by turning it into cashflow. Plus you don’t blow 6% on closing costs, and it’s all the same to the bank in terms of getting another loan. It actually ends up being an equity asset as well as income.

Err, what I meant to say was murder all landlords.

It’s possible, if you have the savings for a second down payment. I’m pretty sure you also lose certain tax advantages if you convert your primary home to an income property. Depending on how long you’ve owned it, that can work out to a serious hit.

You can’t deduct the mortgage interest (you can on the new primary residence though), but suddenly every dollar you spend on the rental property is tax deductible as a business expense. And you can like deduct depreciation on the appliances and shit. It’s actually more tax advantaged in some situations.

Bought my house just before the crash in 2007. Felt screwed over as I went underwater and was stuck with my 6.5% loan while interest rates and home values plummeted (and because my mortgage was privately held, no HARP refi option.

Finally after nearly 15 years not only go out from under water but built enough equity for a no cost refinance. Got into a 2.25% loan.

Sad part is, despite the lower rate, due to skyrocketing insurance and taxes, my payment is no cheaper

I suspect when rates go down, there will be a new rush for people wanting to change properties. That means new high demand for houses and another jump in valuation.

It will likely never get to 4% again unless there is another major recession or you are willing to get an ARM. Historically, 4% is extremely rare for fixed rate mortgages.

7-8% rates are bad by recent standards but not awful by historical standards. Depending on where I move and how much house I can get, I’d be willing to give up my 2.9% rate for something in that range.

There are a few other factors to consider right now, anyway. I’m a Houston resident, and this is supposed to be a particularly bad hurricane season along with a historic heat wave. My wife is terrified of the state’s newest right wing legislative push, as well. Michigan, Minnesota, and Washington is looking better and better as Texas brains are poisoned by MAGA media. And, despite having a gangbusters growth, my O&G employer decided to cut our bonuses from last year - so I’ve got one eye on the job market again. Our water bill jumped by 9% in a single year. Our interior roadways are falling apart, with no sign that the city or state plans to clean them up or improve access to public transit. HISD is being cannibalized by the governor’s cronies, so I won’t have anywhere to send my kids in a few years.

Would I pay an extra $500/mo to live in a state that isn’t run by pedophiles, bigots, and zealots? Absolutely. Bonus points if it got me out of the concrete jungle and put me in spitting distance of some decent mass transit.

If those are your problems with your area then you might as well just leave the US, we’re not getting mass transit anytime soon, climate change will make weather and necessities more expensive everywhere, and fascists are one lucky election away from bringing forth Gilead

A lot of Texans are thinking about it. My mother is deeply a-political, she retired last year, but she told me a year ago that if I needed to move to the Netherlands she would move to help me. (Her grandparents were dutch immigrants, so she might qualify for citizenship where I wouldn’t.)

The dropping interest rate is one of the main reasons that housing prices have skyrocketed in the past 20 years. People judge housing prices by what they can afford monthly and interest rates directly impact that figure. It’s only a matter of time for housing prices to fall drastically if interest rates remain at 7%.

And yes, I have a 500k loan at 2.5% on a 30yr fixed mortgage. Maybe we’ll sell our house in 15 years, but otherwise, forget it! I have zero interest in paying it off early.

Actual deflation is unlikely. You might see a kind of stagflation where prices drop relative to real inflation, but an actual widespread drop in home prices has literally occurred once in the past hundred years, and that was in 2008.

When we were buying (2019), my in-laws were pushing for us to just get a starter home, and then upgrade in a few years. Both my wife and I were like “no, we’re buying once and being done with.” So we went a little higher than I was comfortable with.

However, our house has increased by 50% since we bought it, and we were able to refinance to 3% during the pandemic. Which was and is fantastic. But, yeah, we don’t even think about moving now.

Add comment